How to Diversify Your Mutual Fund Portfolio (And Why It Matters More Than Ever)

Many investors believe they are diversified — until the market falls.

Owning 5–6 mutual funds may feel like diversification, but in reality, many portfolios are heavily concentrated in the same sectors, stocks, or strategies. This creates hidden risk that only shows up during market volatility.

The problem is simple: most investors don’t know what true diversification looks like.

In this guide, we’ll break down what diversification actually means, how to diversify your mutual fund portfolio properly, and how to avoid common mistakes that can silently reduce your returns.

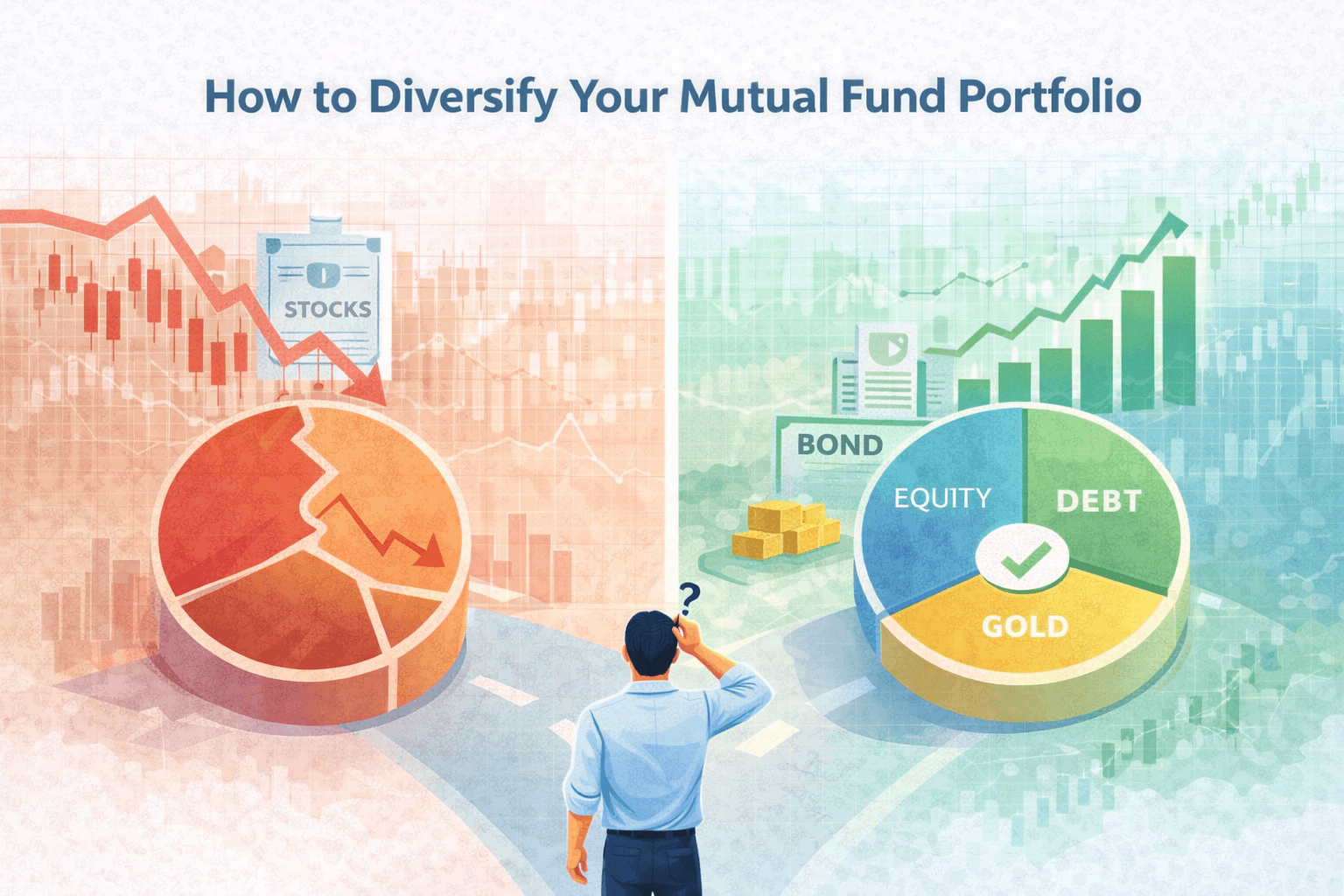

What Is Diversification?

Diversification is the process of spreading your investments across different types of assets to reduce risk.

Instead of putting all your money into one type of investment (like equity), you distribute it across:

- Equity (growth)

- Debt (stability)

- Gold (hedge)

- Liquid funds (emergency)

Within equity itself, diversification means investing across:

- Large cap companies

- Mid cap companies

- Small cap companies

The idea is simple:

When one part of your portfolio performs poorly, another part can help balance it.

What Does a Non-Diversified Portfolio Look Like?

Many investors think they are diversified when they are not.

For example:

- 3 large cap funds

- 2 flexi cap funds

- 1 index fund

This may look diversified, but often all these funds hold similar stocks like Reliance, HDFC Bank, Infosys, etc.

So in reality, the portfolio is concentrated, not diversified.

Comparison Framework

| Factor | Poorly Diversified Portfolio | Well Diversified Portfolio |

|---|---|---|

| Risk | High (hidden concentration) | Balanced across assets |

| Volatility | Sharp ups & downs | Smoother performance |

| Downside Protection | Weak | Stronger |

| Return Consistency | Unstable | More predictable |

| Emotional Stress | High | Lower |

Diversification doesn’t eliminate risk — it manages it better.

How to Diversify Mutual Fund Portfolio Properly

Diversification happens at 3 levels.

1. Asset Class Diversification

This is the most important layer.

A balanced portfolio may include:

- Equity (50–70%) → growth

- Debt (20–40%) → stability

- Gold (5–10%) → hedge

Why this matters:

- Equity grows wealth

- Debt reduces volatility

- Gold protects during uncertainty

2. Market Cap Diversification (Within Equity)

Within equity funds, diversify across:

- Large cap → stability

- Mid cap → growth

- Small cap → high potential

A common structure:

- 50% large cap

- 30% mid cap

- 20% small cap

3. Strategy Diversification

This includes mixing different fund types:

- Index funds

- Actively managed funds

- Sector exposure (limited)

- Hybrid funds

This reduces dependency on a single strategy.

Real Numbers: Why Diversification Matters

Let’s compare two investors.

Investor A: Concentrated Portfolio

-

100% equity (mid & small caps)

- Monthly SIP: ₹20,000

- Return assumption: 14%

Investor B: Diversified Portfolio

-

60% equity

- 30% debt

- 10% gold

- Monthly SIP: ₹20,000

- Return assumption: 11%

After 15 Years

| Investor | Corpus | Volatility |

|---|---|---|

| A (Concentrated) | ₹1.0–1.1 Cr | Very High |

| B (Diversified) | ₹80–85 L | Moderate |

Now here’s the real difference:

During a market crash:

- Investor A may see 40–50% drawdown

- Investor B may see 15–25% drawdown

Most investors behave like Investor A — but emotionally react like Investor B.

That mismatch leads to panic selling.

Mistakes Investors Make

1. Over-Diversification

Owning 10–15 funds does not mean diversification.

It often leads to:

- duplication

- confusion

- poor tracking

2. Investing in Similar Funds

Many funds overlap heavily.

Example:

- Large cap + flexi cap + index fund → same stocks

3. Ignoring Debt Allocation

Investors chase returns and ignore stability.

This increases panic during market falls.

4. Chasing Sector Funds

Sector/thematic funds can be risky if over-allocated.

They should not dominate your portfolio.

5. Not Rebalancing

Over time:

- equity may increase after a bull run

- risk rises silently

Rebalancing is essential.

What Should YOU Do?

If You Are Under 30

Focus on growth, but still diversify:

- 70% equity

- 20% debt

- 10% gold

If You Are 30–45

Balance becomes critical:

- 60% equity

- 30% debt

- 10% gold

If You Are Nearing Retirement

Focus on stability:

- 40% equity

- 50% debt

- 10% gold

The biggest investing mistake is not lack of returns.

It is lack of structure.

Many investors take high risk unknowingly during bull markets — and then panic during corrections.

Diversification doesn’t just protect your money.

It protects your behavior.

Because a portfolio you can stick with is always better than one that looks perfect on paper.

Why Manual Diversification Is Hard

Diversification sounds simple.

But in reality, it requires:

- choosing the right funds

- deciding allocation

- avoiding overlap

- tracking performance

- rebalancing regularly

Most investors don’t have the time or expertise to do this consistently.

This is why many investors are moving toward structured multi-asset portfolios that automatically diversify across equity, debt, and gold.

These portfolios:

- reduce concentration risk

- adjust allocation over time

- maintain discipline

- remove emotional decisions

Instead of managing multiple funds manually, investors follow a system-driven approach.

What Should You Do Next?

Step 1: List all your current investments

Check for overlap and concentration.

Step 2: Decide asset allocation

Not just funds — focus on categories.

Step 3: Reduce unnecessary funds

Simplify your portfolio.

Step 4: Review annually

Rebalance based on market movements.

If you want to avoid managing diversification manually, you can explore structured portfolio approaches that handle allocation and rebalancing automatically.

FAQ

1. What is diversification in mutual funds?

Diversification means spreading investments across different fund types and asset classes to reduce overall risk.

2. How many mutual funds should I have?

Typically, 4–6 funds are enough if properly diversified.

3. Can diversification reduce returns?

It may slightly reduce peak returns but improves consistency and risk-adjusted returns.

4. Should I diversify within equity only?

No. True diversification includes equity, debt, and other assets like gold.

5. How often should I rebalance my portfolio?

At least once a year or when allocation deviates significantly.

6. Is diversification enough to protect from losses?

No strategy eliminates risk completely, but diversification significantly reduces impact during market downturns.