Why Your Mutual Fund Portfolio Is Not Growing (Even After Years of Investing)

You’ve done everything “right.”

You started your SIP.

You stayed consistent.

You ignored short-term noise.

And yet… your portfolio isn’t growing the way you expected.

If that sounds familiar, you’re not alone.

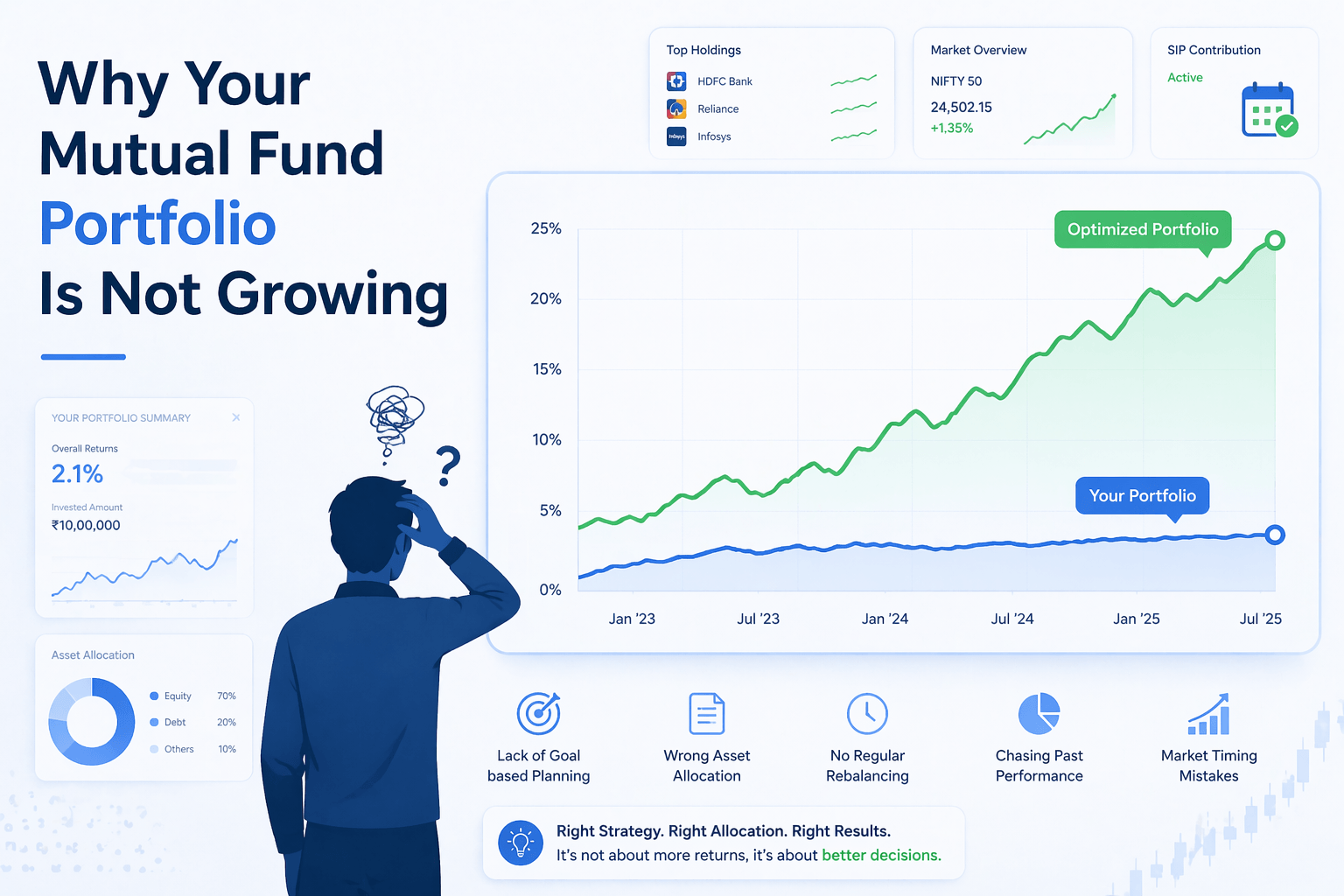

Millions of Indian investors are investing regularly—but not necessarily correctly. The gap between effort and outcome often comes down to strategy, structure, and discipline.

This blog breaks down exactly why your mutual fund portfolio is underperforming—and how to fix it.

Quick Reality Check

Your portfolio may not be growing because:

- You selected average or underperforming funds

- Your portfolio has hidden overlap

- You never rebalance

- You misunderstand market cycles

- You believe SIP alone guarantees returns

SIP is a method—not a strategy.

The Biggest Myth: SIP = Guaranteed Wealth

SIPs are powerful—but they are not magic.

Think of SIP like going to the gym.

Showing up matters—but what you do inside matters more.

The truth:

- SIP ensures discipline

- SIP reduces timing risk

- BUT… SIP does NOT fix poor fund selection

Example:

- ₹5,000/month SIP for 15 years at 10% → ₹20.6 lakh

- Same SIP at 14% → ₹31.2 lakh

That’s a ₹10+ lakh difference—just based on fund quality. Calculate your SIP returns

What’s Actually Going Wrong?

1. Poor Fund Selection (The Silent Killer)

Most investors choose funds based on:

- Last year’s returns

- App rankings

- Friend recommendations

This leads to:

- Performance chasing

- Buying at peaks

- Inconsistent returns

A fund that performed well last year may underperform next year.

2. The Overlap Trap (Fake Diversification)

You think you’re diversified.

But your portfolio might look like this:

- Large Cap Fund A

- Large Cap Fund B

- Flexi Cap Fund

- Index Fund

Sounds good?

Look deeper—and you’ll find the same stocks:

- HDFC Bank

- Reliance

- Infosys

- ICICI Bank

You’re not diversified. You’re duplicated.

Many large-cap funds have 60–70% overlap.

3. Too Many Funds = Diluted Returns

Owning 8–12 funds feels “safe.”

In reality, it creates:

- Confusion

- Overlap

- Average returns

More funds ≠ better performance

✔ Ideal portfolio: 4–6 well-structured funds

4. No Rebalancing = Hidden Risk

Markets move. Your portfolio shifts.

Example:

- Started with 60% equity

- Bull market → now 75% equity

Now your risk is higher—without realizing it.

Without rebalancing:

- Risk increases

- Volatility rises

- Corrections hit harder

5. Misunderstanding Market Cycles

Markets don’t grow in straight lines.

They move in cycles:

- Bull phase → strong returns

- Sideways phase → slow growth

- Bear phase → temporary losses

Many investors:

- Expect constant returns

- Panic during flat phases

- Exit at the wrong time

Wealth is built across cycles—not within one phase.

6. Expense Ratios & Fees (The Invisible Leak)

A small difference in fees creates massive long-term impact.

Example:

- 12% return with 2.5% expense → ₹1.69 Cr

- 12% return with 0.5% expense → ₹2.10 Cr

Difference: ₹41 lakh

Also:

- Regular plans = higher commissions

- Direct plans = lower cost

Over time, fees quietly destroy wealth.

7. No Goal = No Direction

Most investors:

- Don’t know why they’re investing

- Don’t know how much they need

- Keep changing strategy

Investing without goals is like driving without a destination.

8. Emotional Decisions (The Biggest Destroyer)

- Stop SIP during crash❌

- Invest more during market highs ❌

- Switch funds frequently ❌

Research shows:

Investors earn 2–3% less than actual fund returns → purely due to behavior

👉 The problem is rarely the market.

👉 It’s usually the investor.

Real Comparison: Same SIP, Different Outcomes

| Investor | Strategy | Return | Corpus (20 yrs) |

|---|---|---|---|

| A | Random funds, no review | 9–10% | ₹1.1–1.2 Cr |

| B | Structured portfolio | 12–13% | ₹1.6–1.8 Cr |

Difference: ₹40–60 lakh

Same investment. Different approach.

How to Fix Your Portfolio (Action Plan)

The Smart Way

Most investors struggle with:

- Choosing the right funds

- Avoiding overlap

- Knowing when to rebalance

👉 That’s exactly where Algrow by 5nance helps.

What Algrow does:

-

✅ Builds a Goal-based Mutual Fund Portfolio

- ✅ Uses AI to optimize fund selection

- ✅ Automatically identifies overlap & inefficiencies

- ✅ Helps you Rebalance based on market conditions

Instead of guessing, you get a data-driven portfolio that actually works.

Try Algrow

or you can do it manually by following these steps:

Step 1: Audit Your Portfolio

Check:

- Number of funds

- Overlap

- Expense ratios

- Returns vs benchmark

Step 2: Simplify

- Reduce to 4–6 funds

- Remove duplication

Step 3: Allocate Properly

Think in asset allocation, not fund names:

- Equity (growth)

- Debt (stability)

- Gold (hedge)

Step 4: Rebalance Regularly

- Once a year minimum

- Or when allocation shifts >10%

Step 5: Align With Goals

Define:

- What you need

- When you need it

Then invest accordingly.

Step 6: Control Behavior

- Don’t chase returns

- Don’t panic sell

- Don’t over-monitor

Discipline beats intelligence in investing.

Why This Problem Is Growing in India

- Record SIP participation (₹20,000+ crore monthly inflows)

- 2000+ mutual fund schemes

- Information overload

Result:

People are investing more…

But optimizing less.

The Smarter Way Forward

Managing:

- Fund selection

- Allocation

- Rebalancing

…manually is complex.

That’s why modern investors are shifting towards:

- Structured Multi-asset Portfolios

- Data-driven allocation

- AI based rebalancing

The focus is shifting from “which fund” → “how the portfolio works together”

Final Thought

The uncomfortable truth:

- Your portfolio isn’t underperforming because of the market.

- It’s underperforming because of how it’s built and managed.

The good news?

That’s completely fixable.

What Should You Do Next?

Don’t guess.

Don’t assume.

Check if your portfolio is actually working for you.

- Are your funds aligned with your goals?

- Are you overpaying in fees?

- Is your allocation optimized?

Fixing these today can mean lakhs more in the future.

FAQs

1. Why is my SIP not giving good returns?

Because returns depend on fund quality, allocation, and behavior—not SIP alone.

2. How many mutual funds should I have?

Typically 4–6 funds are enough if properly diversified.

3. Should I exit underperforming funds?

Yes—but only after evaluating long-term performance and strategy fit.

4. How often should I review my portfolio?

Every 6–12 months.

5. Can too much diversification hurt returns?

Yes. Over-diversification leads to duplication and average outcomes.

Disclaimer

Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. This content is for educational purposes only and not investment advice.